Secure Website

Secure Website

Secure Website

Secure Website

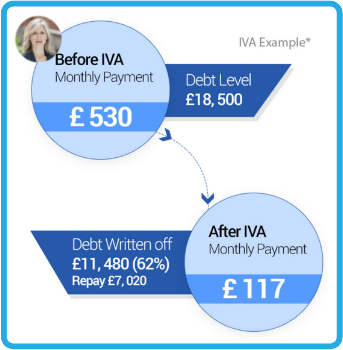

An IVA stands for an Individual Voluntary Arrangement. It is a Formal arrangement set out between you and the unsecured creditors, (credit cards, loans, store cards, catalogues etc). You will make affordable monthly payments, usually over 5 or 6 years, after which the debts included in your IVA will be cleared. An IVA can only be set up by a certified IP (Insolvency Practitioner). The IP will deal directly with your creditors and support you for the full 60 month period.

Start your journey by completing the form.

Debt Management Plans are designed to help those who may not be able to afford the full monthly payments on their accounts but are in a position to make a lower payment on a regular basis. After completing a fact find of your income and outgoings we will be able to identify exactly how much you can reasonably afford to put aside for your creditors.

A Debt Relief Order (DRO) is a very useful debt solution introduced by the government in 2009 and is designed to provide a fresh start for those with less than £20,000 of debt and no assets of value.

DROs work in a very similar way to Bankruptcy although it is seen as a far simpler process with smaller amounts of mo

ney being written off to safeguard your financial future. Each DRO lasts for just one year, at which point you will be free from debt and the associated stresses.

Bankruptcy is a legal process through which people who cannot repay debts to their creditors may seek relief from some or all of their debts. Bankruptcy is often seen as the last resort, but for those with severe debt problems, this can be a lifeline.

The bankruptcy process begins with a petition filed by the debtor, which is most common, or on behalf of creditors, which is less common. All of the debtor’s assets are measured and evaluated, and the assets may be used to repay a portion of outstanding debt.